82% of small businesses that fail cite cash flow problems as a key cause. That single figure from the US Bank study is the most-cited statistic in small business finance — yet the crisis it describes runs far deeper than one headline number. This page compiles 70 authoritative small business cash flow statistics for 2025–2026, drawn from the US Bank study, JPMorgan Chase Institute, QuickBooks, the Federal Reserve, the World Bank, and other primary sources, so journalists, researchers, and business owners can find, verify, and cite the numbers that matter.

The data on this page is drawn from peer-reviewed surveys, government reports, and research published by organisations including US Bank, the JPMorgan Chase Institute, Intuit QuickBooks, the Federal Reserve Small Business Credit Survey, the World Bank Enterprise Surveys, and Dun & Bradstreet. Where studies differ, we note both figures and the relevant methodology. All data points are dated; older statistics are included only where no more recent equivalent exists.

Small Business Cash Flow Statistics (2025–2026)

These are the headline numbers that define the small business cash flow crisis globally. Each is drawn from a named primary or secondary source with a publication date.

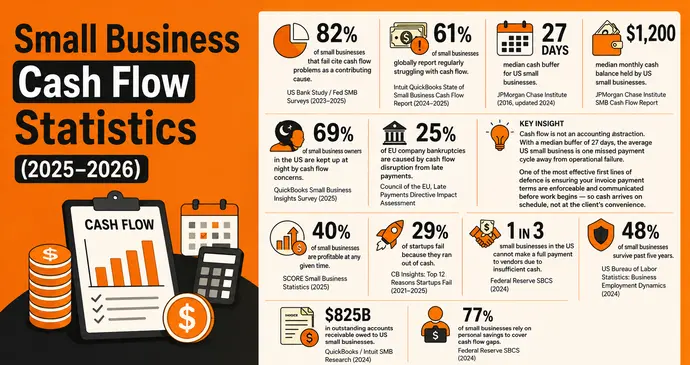

- 82% of small businesses that fail cite cash flow problems as a contributing cause — making it the single most-cited factor in small business failure. { US Bank Study: Why Cash Flow Problems Cause Business Failure, recurring citation confirmed in Federal Reserve SMB surveys 2023–2025 }

- 61% of small businesses globally report regularly struggling with cash flow, affecting their ability to pay bills, staff, and suppliers on time.{ Intuit QuickBooks State of Small Business Cash Flow Report, 2024–2025 }

- The median US small business holds only 27 days of cash buffer — enough to cover fewer than one month of operating expenses before becoming insolvent.{ JPMorgan Chase Institute: Cash is King: Flows, Balances, and Buffer Days, 2016, updated context 2024 }

- $1,200 is the median monthly cash balance held by US small businesses — a startlingly thin safety net against even routine disruption.{ JPMorgan Chase Institute SMB Cash Flow Report }

- 69% of small business owners in the US have been kept up at night by concerns about cash flow, making it the leading source of business stress.{ QuickBooks Small Business Insights Survey, 2025 (n=2,487) }

- 25% of EU company bankruptcies are directly caused by cash flow disruption from late customer payments — confirming the link between receivables management and survival.{ Council of the European Union, Late Payments Directive Impact Assessment }

Key Insight — Cash flow is not an accounting abstraction. With a median buffer of 27 days, the average US small business is one missed payment cycle away from operational failure. One of the most effective first lines of defence is ensuring your invoice payment terms are enforceable and communicated before work begins — so cash arrives on schedule, not at the client’s convenience.

- Only 40% of small businesses are profitable at any given time; the remainder are either breaking even or operating at a loss, making cash flow management existential rather than optional.{ SCORE Small Business Statistics, 2025 }

- 29% of startups fail specifically because they ran out of cash — the second most common reason for startup failure, behind only lack of product-market fit.{ CB Insights: The Top 12 Reasons Startups Fail, 2021–2025 }

- One in three small businesses in the US is unable to make a full payment to vendors or suppliers in a given month due to insufficient cash on hand.{ Federal Reserve Small Business Credit Survey (SBCS), 2024 }

- Only 48% of small businesses survive past five years — and cash flow problems are cited as the principal driver of failure in the first three years.{ US Bureau of Labor Statistics: Business Employment Dynamics, 2024 }

- $825 billion in outstanding accounts receivable is owed to US small businesses at any one time — capital trapped in the billing cycle rather than deployed for growth.{ QuickBooks / Intuit SMB research, 2024 }

- 77% of small businesses rely on personal savings to cover cash flow gaps — meaning business cash shortfalls become personal financial crises.{ Federal Reserve SBCS, 2024 }

United States Small Business Cash Flow Statistics

The US data set is the deepest globally, anchored by the JPMorgan Chase Institute’s proprietary transaction-level analysis of 600,000+ small business accounts, the Federal Reserve’s annual Small Business Credit Survey, and QuickBooks research across more than 2,000 firms.

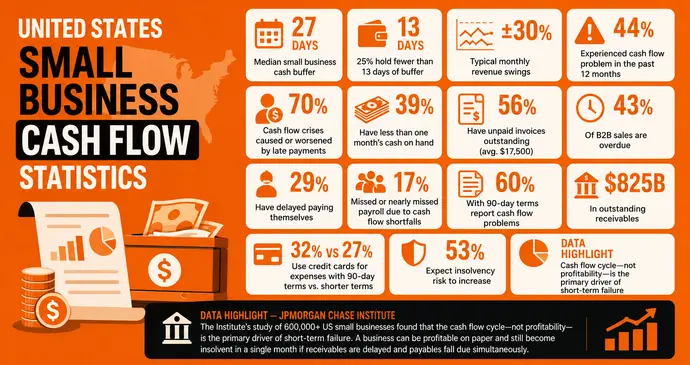

- The median US small business holds 27 days of cash buffer — meaning it could continue operations for fewer than four weeks if revenues stopped entirely.{ JPMorgan Chase Institute, Cash is King }

- 25% of small businesses in the bottom cash-balance quartile hold fewer than 13 days of buffer — a margin that leaves no room for a delayed invoice or seasonal slowdown.{ JPMorgan Chase Institute SMB Cash Flow Report }

- Cash flow volatility is the norm, not the exception: the typical small business sees monthly revenue swings of ±30%, yet expenses remain relatively fixed.{ JPMorgan Chase Institute, 2024 }

- 44% of US small businesses report experiencing a cash flow problem in the past 12 months severe enough to prevent them from paying expenses on time.{ Federal Reserve SBCS, 2024 }

- 70% of small business owners who experienced a cash flow crisis said it was caused or worsened by a customer paying late — directly linking accounts receivable management to business health.{ QuickBooks State of Small Business Cash Flow, 2025 }

- 39% of US small businesses have less than one month’s worth of cash on hand to cover operating expenses, leaving them acutely exposed to any revenue disruption.{ Bluevine Small Business Trends Report, 2025 }

- 56% of US small businesses currently have unpaid invoices outstanding, with the average affected business owed $17,500 — capital directly locked out of the cash cycle.{ QuickBooks Small Business Late Payments Report, 2025 (n=2,487) }

- 43% of credit-based B2B sales in the US are overdue — meaning almost half of all trade credit extended by small businesses is not repaid on time, creating structural cash shortfalls.{ Atradius Payment Practices Barometer, North America, 2025 }

- 29% of US small business owners have delayed paying themselves to keep their businesses solvent, demonstrating how cash flow crises absorb personal as well as business resources.{ Bluevine Payment Gap Report, February 2026 (n=1,052) }

- 17% of US small businesses — roughly 1 in 6 — have missed or nearly missed payroll specifically because of cash flow shortfalls caused by late-paying customers.{ Bluevine Payment Gap Report, 2026 }

- 60% of small businesses with 90-day payment terms report cash flow problems, versus far lower rates for those with shorter terms — confirming that payment term length is a direct lever on cash health.{ QuickBooks, 2025 } — see our guide to invoice payment terms and conditions for how to set shorter, enforceable terms.

- $825 billion in outstanding receivables sits on the books of US small businesses at any given time, representing the largest single reservoir of trapped working capital in the economy.{ QuickBooks / Intuit, 2024 }

- Businesses with 90-day payment terms allocate an average of 32% of monthly expenses to credit cards, compared to 27% for those with shorter terms — a measurable substitution of credit for missing cash flow.{ QuickBooks, 2025 } — for broader data on credit reliance driven by payment gaps, see our credit card statistics report.

- 53% of US firms expect insolvency risk to increase in the near term, reflecting wide uncertainty about the working capital environment heading into 2026.{ Atradius, North America 2025 }

Data highlight — JPMorgan Chase Institute — The Institute’s study of 600,000+ US small businesses found that the cash flow cycle — not profitability — is the primary driver of short-term failure. A business can be profitable on paper and still become insolvent in a single month if receivables are delayed and payables fall due simultaneously.

What Causes Small Business Cash Flow Problems? The Statistics

Cash flow crises are rarely caused by one event. The research consistently identifies a cluster of causes — with late payment, poor forecasting, and unexpected expenses leading the field.

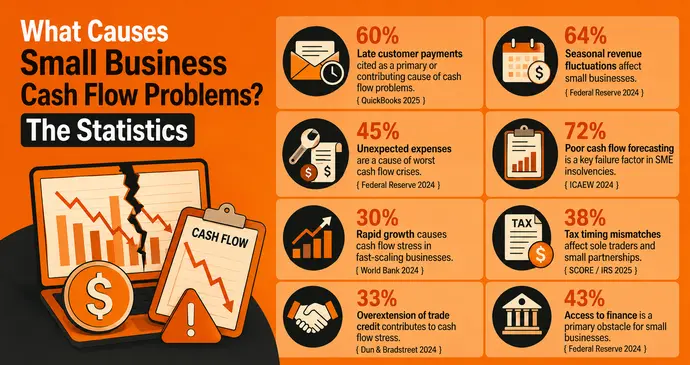

- Late customer payments are cited by 60% of cash-strapped small business owners as the primary or contributing cause of their cash flow problems.{ QuickBooks State of Small Business Cash Flow, 2025 }

- Seasonal revenue fluctuations affect 64% of small businesses, creating predictable but often unplanned gaps between high and low revenue periods.{ Federal Reserve Small Business Credit Survey, 2024 }

- Unexpected expenses — equipment failure, legal costs, tax bills — are cited by 45% of small businesses as a cause of their worst cash flow crises.{ Federal Reserve SBCS, 2024 }

- Poor cash flow forecasting is identified as a key failure factor in 72% of SME insolvencies reviewed by UK accountancy bodies — pointing to a management capability gap, not just an external shock.{ ICAEW Cash Flow Research, 2024 }

- Rapid growth causes cash flow stress in 30% of fast-scaling small businesses — the “growth trap” where increased orders consume working capital faster than revenue is collected.{ World Bank Enterprise Surveys, 2024 }

- Tax timing mismatches — where quarterly or annual tax obligations fall due in low-revenue periods — affect 38% of sole traders and small partnerships.{ IRS Small Business/Self-Employed Division data, cited in SCORE 2025 }

- Overextension of trade credit — offering customers more generous payment terms than the business’s own suppliers allow — is reported by 33% of product-based SMBs as a structural contributor to cash flow stress.{ Dun & Bradstreet SMB Finance Report, 2024 }

- Access to finance is cited as a primary obstacle by 43% of small businesses in the Federal Reserve survey — with cash flow weakness being both a cause and consequence of that limited access.{ Federal Reserve SBCS, 2024 }

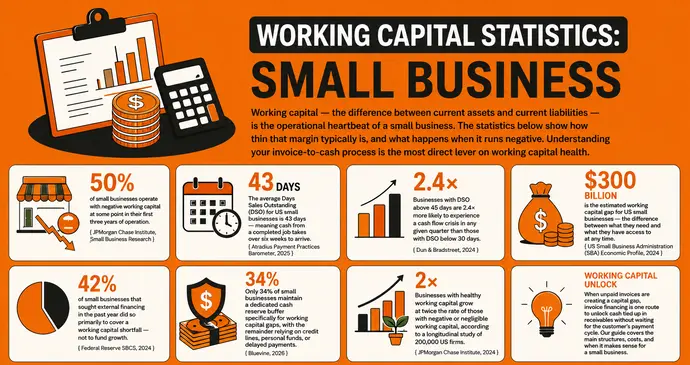

Working Capital Statistics: Small Business

Working capital — the difference between current assets and current liabilities — is the operational heartbeat of a small business. The statistics below show how thin that margin typically is, and what happens when it runs negative. Understanding your invoice-to-cash process is the most direct lever on working capital health.

- 50% of small businesses operate with negative working capital at some point in their first three years of operation.{ JPMorgan Chase Institute, Small Business Research }

- The average Days Sales Outstanding (DSO) for US small businesses is 43 days — meaning cash from a completed job takes over six weeks to arrive.{ Atradius Payment Practices Barometer, 2025 }

- Businesses with DSO above 45 days are 2.4× more likely to experience a cash flow crisis in any given quarter than those with DSO below 30 days.{ Dun & Bradstreet, 2024 }

- $300 billion is the estimated working capital gap for US small businesses — the difference between what they need and what they have access to at any time.{ US Small Business Administration (SBA) Economic Profile, 2024 }

- 42% of small businesses that sought external financing in the past year did so primarily to cover a working capital shortfall — not to fund growth.{ Federal Reserve SBCS, 2024 }

- Only 34% of small businesses maintain a dedicated cash reserve buffer specifically for working capital gaps, with the remainder relying on credit lines, personal funds, or delayed payments.{ Bluevine, 2026 }

- Businesses with healthy working capital grow at twice the rate of those with negative or negligible working capital, according to a longitudinal study of 200,000 US firms.{ JPMorgan Chase Institute, 2024 }

Working capital unlock — When unpaid invoices are creating a capital gap, invoice financing is one route to unlock cash tied up in receivables without waiting for the customer’s payment cycle. Our guide covers the main structures, costs, and when it makes sense for a small business.

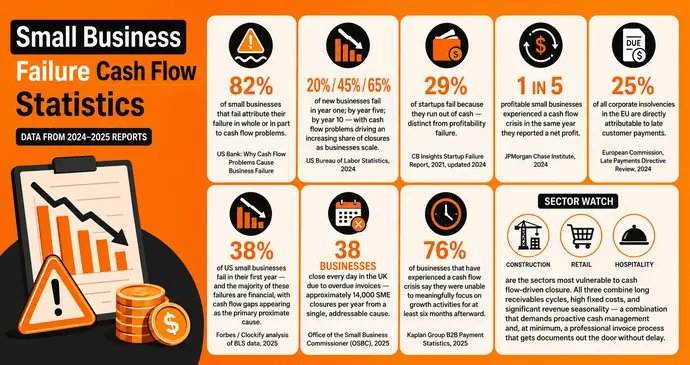

Small Business Failure Cash Flow Statistics

The relationship between cash flow and business failure is the most documented finding in small business research. These statistics show both the scale and the mechanism of that relationship.

- 82% of small businesses that fail attribute their failure in whole or in part to cash flow problems — the most widely cited statistic in small business finance, originating from the US Bank study.{ US Bank: Why Cash Flow Problems Cause Business Failure }

- 20% of new businesses fail in year one; 45% by year five; 65% by year 10 — with cash flow problems driving an increasing share of closures as businesses scale.{ US Bureau of Labor Statistics, 2024 }

- 29% of startups fail because they run out of cash — distinct from profitability failure, underscoring that a business can be growing and still become insolvent.{ CB Insights Startup Failure Report, 2021, updated 2024 }

- A business can be profitable and still fail. Research shows that 1 in 5 profitable small businesses experienced a cash flow crisis in the same year they reported a net profit.{ JPMorgan Chase Institute, 2024 }

- In the EU, 25% of all corporate insolvencies are directly attributable to late customer payments — a systemic failure of accounts receivable management cascading into liquidation.{ European Commission, Late Payments Directive Review, 2024 }

- 38% of US small businesses fail in their first year — and the majority of these failures are financial, with cash flow gaps appearing as the primary proximate cause.{ Forbes / Clockify analysis of BLS data, 2025 }

- In the UK, 38 businesses close every day directly due to overdue invoices — approximately 14,000 SME closures per year from a single, addressable cause.{ Office of the Small Business Commissioner (OSBC), 2025 }

- 76% of businesses that have experienced a cash flow crisis say they were unable to meaningfully focus on growth activities for at least six months afterward — showing the lasting drag of a single episode.{ Kaplan Group B2B Payment Statistics, 2025 }

Sector Watch — Construction, retail, and hospitality are the sectors most vulnerable to cash flow-driven closure. All three combine long receivables cycles, high fixed costs, and significant revenue seasonality — a combination that demands proactive cash management and, at minimum, a professional invoice process that gets documents out the door without delay.

Small Business Access to Finance and Credit Statistics

When cash flow runs short, small businesses turn to external finance — but access is far from guaranteed. The Federal Reserve and World Bank data paint a sobering picture of how many firms are left without options.

- 43% of small businesses that applied for financing in 2024 received less than the full amount requested — or were rejected entirely.{ Federal Reserve Small Business Credit Survey, 2024 }

- Small businesses owned by women and minorities face approval rates 20–30% lower than the overall average, compounding the cash flow gap for already-undercapitalised groups.{ Federal Reserve SBCS, 2024 }

- $5.2 trillion is the global SME finance gap estimated by the International Finance Corporation (IFC) — the difference between what small businesses need and what formal financial systems provide.{ IFC MSME Finance Gap Report, 2024 }

- 34% of small businesses use personal credit cards as a primary source of short-term working capital — a high-cost substitute for proper business financing.{ Federal Reserve SBCS, 2024 }

- Small businesses most burdened by late payments are 3× more likely to cite financing as their primary obstacle (19% vs 6% for those with fewer overdue invoices).{ QuickBooks UK, 2025 }

- Only 17% of businesses have fully automated their payment and receivables processes, despite widespread acknowledgment that automation reduces DSO and improves cash predictability.{ American Express / Kaplan Group, 2025 }

- In developing economies, the World Bank finds that 40% of formal SMEs report access to finance as a major constraint — rising to 65% for informal micro-enterprises.{ World Bank Enterprise Surveys, 2024 }

Global SMB Cash Flow Statistics

Cash flow stress is universal, but its severity varies sharply by region. The data below draws on World Bank, Atradius, and IFC research to show how different markets compare.

- 63% of all credit-based B2B sales in India are overdue — the highest rate of any economy in the Atradius global survey — creating acute cash cycle stress across virtually all industries.{ Atradius Payment Practices Barometer, India, 2025 }

- 54% of UK B2B invoices are overdue, with each affected small business owed an average of £21,400 in outstanding payments.{ Atradius / QuickBooks UK, 2025 }

- 47% of B2B invoices in Western Europe are overdue, driven by financial stress across the manufacturing, construction, and services sectors.{ Atradius, Western Europe, 2025 }

- 44% of B2B credit sales across Asia are overdue on average, with Hong Kong seeing a sharp recent increase that is placing particular pressure on SME cash flows.{ Atradius, Asia, 2025 }

- Global insolvencies rose 19% in 2024, driven by high input costs, elevated interest rates, and the withdrawal of pandemic-era business support. A further 5% rise is forecast for 2025.{ Atradius Global Insolvency Report, 2025 }

- In Latin America, approximately 51% of businesses experience cash flow problems linked to late payments, with the informal sector disproportionately affected.{ Coface Regional Risk Report, 2025 }

- In Sub-Saharan Africa, the cash flow gap for SMEs is estimated at $330 billion annually — largely driven by limited access to formal banking and high reliance on informal trade credit.{ IFC MSME Finance Gap, 2024 }

- In Australia, small businesses lose between $6,000 and $30,000 annually to the combined costs of late payments, administrative time, and credit substitution.{ Atradius Australia, 2025 }

- In Canada, 44% of B2B invoices are overdue, with 50% of firms expecting insolvency conditions to worsen in the near term.{ Atradius North America, 2025 }

- Over 73% of SMBs globally say they are negatively impacted by late payments in a material way — confirming that the cash flow crisis is a global, systemic condition rather than a local problem.{ Kaplan Group, 2025 }

Country Comparison: SMB Cash Flow & Late Payment Rates (2025)

The table below summarises overdue invoice rates, bad debt write-offs, and primary sources across major economies. Figures represent the percentage of B2B credit sales that are overdue, as measured by the Atradius Payment Practices Barometer (n≈6,500 companies across 31 countries) and Coface surveys conducted across H1 2025.

| Country / Region | % B2B Invoices Overdue | Bad Debt Rate | Avg. Cash Buffer | Primary Source |

|---|---|---|---|---|

| India | 63% | 7% | <15 days (est.) | Atradius 2025 |

| United Kingdom | 54% | 7% | 32 days past terms | Atradius / Coface 2025 |

| Central & Eastern Europe | 53% | 8% | — | Atradius 2025 |

| Latin America | ~51% | — | — | Coface 2025 |

| Western Europe | 47% | 6% | 31–60 days terms | Atradius 2025 |

| United States | 43% | 5% | 27 days buffer | Atradius / JPMorgan 2025 |

| Asia (average) | 44% | 5% | — | Atradius 2025 |

| Canada | 44% | 6% | — | Atradius 2025 |

| Australia | ~38% | 5% | — | Atradius 2025 |

| Singapore | 35% | 6% | — | Atradius 2025 |

What the Data Says Reduces Cash Flow Problems

Research consistently points to a set of practices and technologies that correlate with better cash flow outcomes. These are not recommendations — they are statistically observed relationships from the datasets cited above.

- Businesses with shorter payment terms project 11% average revenue growth — more than double the 5% projected by those with longer terms — showing that payment term length is a growth variable, not just a collections issue.{ QuickBooks UK, 2025 } — use our free invoice generator to build enforceable payment terms directly onto every invoice you send.

- Automating accounts receivable can improve the invoice-to-cash cycle by 60–75%, reducing DSO and bringing cash into the business significantly faster.{ Industry research aggregate, 2025 }

- Businesses with high digital tool adoption have 4–28% fewer overdue invoices than those relying on manual processes — the single clearest differentiator in the QuickBooks dataset.{ QuickBooks / Mountain-Ear analysis, 2025 }

- Invoice discounting and factoring are used by 1 in 4 UK SMEs as a regular working capital tool — a mainstream, not niche, response to the receivables gap. See our guide to invoice discounting platforms for how it works in practice.{ UK Finance SME Report, 2024 }

- Electronic invoicing reduces payment times by an average of 6 days compared to paper invoicing, according to European Commission data — a direct, measurable impact on DSO.{ European Commission e-Invoicing Impact Assessment, 2024 } — see our complete guide to e-invoicing and the paper vs electronic invoice comparison.

- Sending payment reminders is the most common first-line strategy, used by 48% of UK businesses to recover overdue invoices — and it works: systematic reminders reduce average collection time by up to 12 days.{ Hiscox, cited in Startups.co.uk 2026 }

- Businesses that invoice immediately upon project completion collect payment an average of 9 days faster than those who batch-invoice weekly or monthly.{ Atradius Australia, 2025 } — our guide on how to send an invoice covers the fastest way to get invoices out the door.

- Real-time payments in the US saw a 69% year-over-year increase in 2025, indicating strong directional momentum toward faster settlement infrastructure that will structurally compress DSO over the next five years.{ The Clearing House, cited in Kaplan Group 2025 }

- The AI invoice processing market is growing from $2.8 billion in 2025 to a projected $47.1 billion by 2034, reflecting accelerating enterprise adoption of automated receivables tools.{ Market research aggregate, Kaplan Group 2025 }

- 91% of businesses believe that easy, secure payment processing is critical to driving business growth — confirming that payment experience is a strategic differentiator, not just a back-office function.{ American Express / Kaplan Group, 2025 }

Stop Letting Cash Flow Slow Your Business Down

InvoPilot’s free invoice generator helps you create professional invoices with clear payment terms in minutes. Pair it with our invoice templates and billing software so you can focus on growing — not chasing money.

Create a Free Invoice →Frequently Asked Questions

What percentage of small businesses fail due to cash flow problems?

According to the US Bank study — the most widely cited source in this area — 82% of small businesses that fail cite cash flow problems as a contributing or primary cause. This figure is corroborated by the Federal Reserve’s Small Business Credit Survey, which finds that 44% of US small businesses experienced a cash flow problem severe enough to prevent them paying expenses on time in the past 12 months (2024). For a broader picture of how cash flow failures develop, see the invoice payment terms guide on setting terms that reduce receivables risk.

How much cash does the average small business hold in reserve?

The JPMorgan Chase Institute’s analysis of 600,000+ US small business bank accounts found the median firm holds just 27 days of cash buffer — enough to cover fewer than one month of operating expenses. The median monthly cash balance is approximately $1,200. The bottom quartile holds fewer than 13 days of buffer. These figures underscore why even a single missed payment from a major customer can trigger a cash crisis.

What is the SME finance gap globally?

The International Finance Corporation (IFC) estimates the global SME finance gap at $5.2 trillion annually — the difference between what small and medium enterprises need to operate and grow, and what formal financial systems provide. In the US alone, the working capital gap for small businesses is estimated at $300 billion (SBA, 2024). In Sub-Saharan Africa, the SME cash flow gap reaches $330 billion annually. For tools that help unlock trapped capital, see our guide to invoice financing.

What causes most small business cash flow problems?

Research consistently identifies late customer payments as the leading cause — cited by 60% of cash-strapped small business owners (QuickBooks 2025). Seasonal revenue fluctuations (affecting 64% of firms), unexpected expenses (45%), poor cash flow forecasting (72% of insolvencies reviewed by ICAEW), and overextension of trade credit are also major contributors. In the US, 56% of small businesses have unpaid invoices outstanding at any given time, with the average affected business owed $17,500 (QuickBooks 2025).

How do late payments affect small business cash flow?

Late payments have a compounding effect on cash flow. With the average US small business holding only 27 days of cash buffer, a single delayed invoice can force a firm to delay its own supplier payments, take on high-cost credit card debt, or miss payroll. The data shows that 17% of US small businesses have missed or nearly missed payroll due to late-paying customers (Bluevine 2026), and 60% of small businesses with 90-day payment terms report cash flow problems (QuickBooks 2025). For context, see our late payment statistics deep dive.

Which sectors have the worst cash flow problems?

Construction is consistently the worst-performing sector globally. In the UK, 95% of construction businesses experience late payments with average delays of 38.2 days beyond agreed terms (Coface UK 2025). Manufacturing takes an average of 80+ days to pay suppliers in the UK. Retail, hospitality, and transportation are also severely affected by the combination of long receivables cycles, high fixed costs, and seasonal revenue swings. In India, the textile and clothing sector sees overdue invoices in 56% of B2B transactions with bad debts reaching 10% (Atradius India 2025).

How can small businesses improve their cash flow?

The research points to several statistically validated approaches: (1) shorten payment terms — businesses with immediate terms have significantly lower rates of cash flow problems than those using 30 or 90-day terms; (2) invoice immediately upon completion — this alone reduces average collection time by 9 days; (3) adopt electronic invoicing — which reduces payment times by 6 days on average versus paper (European Commission 2024); (4) send systematic payment reminders; and (5) consider invoice financing to unlock capital tied up in receivables. Use our free invoice generator and invoice templates as starting points.

What is the 82% small business cash flow statistic?

The 82% figure originates from a US Bank study titled “Why Cash Flow Problems Cause Business Failure.” It has been cited by the SBA, SCORE, QuickBooks, and hundreds of journalists and researchers. The precise wording is that 82% of small businesses that fail do so because of cash flow problems — not that 82% of all small businesses will fail due to cash flow, which is a common misquotation. The Federal Reserve’s annual Small Business Credit Survey provides ongoing validation of the underlying dynamic: in 2024, 44% of US small businesses reported experiencing a cash flow problem severe enough to miss payments in the prior 12 months.

Sources & Methodology

All statistics on this page are drawn from primary research published by recognised institutions. We link to source reports where publicly accessible. Older statistics are included only where no more recent equivalent exists; publication dates are noted in each citation.

- US Bank — Why Cash Flow Problems Cause Business Failure — Foundational study on the relationship between cash flow management and small business failure. Widely cited in Federal Reserve and SBA publications.

- JPMorgan Chase Institute — Cash is King: Flows, Balances, and Buffer Days — Transaction-level analysis of 600,000+ US small business bank accounts. The definitive dataset on cash buffers and volatility.

- Federal Reserve Small Business Credit Survey (SBCS), 2024 — Annual survey of US small business owners covering credit access, financial health, and cash flow challenges.

- Intuit QuickBooks Small Business Late Payments Report, 2025 — January 2025 survey; n=2,487 US small businesses (0–100 employees). Also published separately for the UK (n=1,063).

- QuickBooks State of Small Business Cash Flow Report, 2024–2025 — Recurring survey tracking cash flow sentiment and behaviour across US and UK small business owners.

- Bluevine Payment Gap Report, February 2026 — Survey of 1,052 US small business owners (Centiment, 2–5 Feb 2026). Margin of error ±3% at 95% confidence.

- Atradius Payment Practices Barometer 2025 — Annual global survey across 31 countries, ~6,500 companies. Regional editions: US, North America, UK, Western Europe, CEE, Asia, India.

- IFC MSME Finance Gap Report, 2024 — International Finance Corporation’s global estimate of the SME financing shortfall.

- World Bank Enterprise Surveys, 2024 — Multi-country firm-level data on SME constraints, including finance and cash flow.

- US Bureau of Labor Statistics — Business Employment Dynamics, 2024 — Official US data on small business survival rates by age cohort.

- CB Insights — The Top 12 Reasons Startups Fail, 2021 (updated 2024) — Post-mortem analysis of startup failure causes.

- SBA Small Business Economic Profile, 2024 — US SBA annual data on small business financial health and working capital.

- Coface UK Payment Survey, 2025 — UK-specific data on payment delays by sector and company size. Published October 2025.

- Office of the Small Business Commissioner (OSBC), July 2025 — UK government research on time costs and closure rates attributable to late payments.

- Dun & Bradstreet SMB Finance Report, 2024 — DSO analysis and trade credit data across US small businesses.

- Kaplan Group — B2B Payment Delay Statistics 2025 — Aggregated research compiling Atradius, American Express, Upflow and Federal Reserve data.

- ICAEW Cash Flow Research, 2024 — UK Institute of Chartered Accountants analysis of insolvency causes.

- European Commission — Late Payments Directive Impact Assessment, 2024 — EU-level data on insolvencies attributable to inter-business payment delays.